- 17 May 2024

Air & Ocean Market Update |

Ocean Freight The Far East West Bound

The Far East West Bound trade is facing a challenging period with various factors contributing to the difficulties currently being experienced by importers and shipping lines including:

Inventory management

Many importers still vividly recall the inventory nightmare they were in right after COVID, with warehouses chuck-full of freight and consumer demand too low to sustain reasonable throughput of freight – this has led to the majority of them being very careful in reordering stock, to avoid that inventory sitting in their warehouse idle. Some of our customers have admitted that they’ve been too careful and have started their usual order process too late – meaning stock levels have decreased to dangerously low levels, and lost sales are becoming a real concern. This leads to some customers now overordering, to compensate for their (lack of) responsiveness. Several of our customers are showing an uptick in bookings of 10-20%.

Transit times

The inventory management issue is magnified by the massive increase in transit times we’re experiencing because of the Red Sea diversions across the Cape of Good Hope – the average increase in transit time still sits around 10-15 days, and it seems that many importers had not accounted for these additional days in their ERP systems. Although shipping lines have been speeding up their vessels, the traditional transit times of 30-35 days from China’s main ports are a fairy tale of the past.

Congestion (at transshipment hubs)

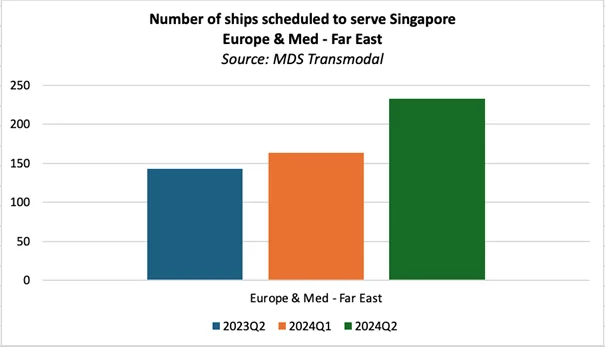

The increase in transit time and deployment of more vessels has led to higher pressure on the traditional transshipment hubs of Singapore, Port Kelang, Tanjung Pelepas and (to a lesser extent) Hong Kong. The below figure shows a 50% increase in vessels calling at Singapore when comparing Q1 numbers to Q2. This also directly impacts other trades, as 50% of the Oceania cargo, for example, moves on these vessels too. In Q1, average dwell time of a container was sitting around 7 days, with that number now increasing to 2 weeks.

Supply / capacity management

Despite the uptick in demand, the carriers are still cautiously managing their available capacity and have learnt that their blank sailing programmes are a very effective tool to manage rate levels. Carriers are understandably keen on keeping rates at their current levels (if not higher), and have vowed to increase their schedule reliability, which means port calls are cut and underperforming services taken out of rotation. There are also a lot of vessels undergoing overdue maintenance (postponed through COVID) and the delayed arrival of some new vessels (because of a lack of demand over Q4 and Q1, after the Cape of Good Hope routing became the new normal) means that new capacity cannot immediately be applied to this trade.

Equipment shortages

If space is not enough of a concern, the equipment pools in (mostly) China are running dry too. The longer transit times and increased congestion mean we see a permanent shortage of containers in the main base ports, and although new (leased) equipment is due to arrive over the next few weeks, this a proverbial drop in the ocean, and we should expect this to be a recurring cyclical issue. The lack of equipment increases the roll-over pool, impacting sailings further ahead for existing and new bookings. This adds yet again more delays to the overall port-to-port transit time for the average container.

Market visibility / intelligence

Last but not least, most of the above-mentioned info is available to read online, in an almost immediate fashion – for everyone. This visibility increases the understanding of the freight market among our customers, but also drives the heavy peaks we now experience: the fact that the tight space situation and equipment issues are known to importers directly, sparks a Pavlov-response to order more stock as far in advance as possible, which in turn means vessels are booked out more than a month ahead of their scheduled ETD – an ongoing vicious circle that is hard to break.Consumer spending across Europe for 2024 is expected to increase by only 1.1%, so the uptick in bookings is not a sign of sustained economic activity, but rather a short-lived boom.

We anticipate these challenges to remain for the short term so don’t hesitate to reach out to your local Mainfreight branch for advice and support with moving your goods.

Do you want to know more?

Get in touch with your local Mainfreight branch for advice and support.

Contact us